Tips for maximizing Credit Card points when furnishing a new house in Singapore

I consider myself a novice points earner. I knew the concept of earning points from credit card (specifically airline miles) and have benefited from redeeming a few flights from my credit card points. But in relative to the points moguls in Singapore, I am just a small fry.

My points-earning strategy is basic at best: I only had one credit card that I use on all of my spending, the DBS Altitude, which doesn’t even earn the best miles per dollar (hereby referred to as “mpd”).

But recently I bought a house, and thus begin the onslaught of furniture buying and furnishing. Being the good auntie that I am, of course I don’t want to miss out on the potential points I can earn from all that spending!

SO, I spent some time revising my credit card points spend, and here’s what I’ve learned:

1. The 10x Rewards Cards is your friend for online purchases

In Singapore, there exists a category of cards that will reward you bonus points. Usually this reward is given for online purchases or shopping at department store — Perfect for home furnishing! Each bank has their own points to miles calculation, but this is usually just marketed as 10x points. Hence these cards have been casually referred to as the “10x cards”.

But if you only care about miles like me, then this just means these cards will earn you 4 mpd for every dollar you spend. For the purpose of this article, I will continue to refer to the bonus points in mpd, since it’s more universal that way.

DBS Woman’s Card, Citigroup Citi Rewards and OCBC Titanium are some of the crowd’s favorite that falls into this category of cards. They all offer the same benefit too, which at first glance makes it a bit confusing to choose which card to get (and i’ll get to that soon).

For comparison, the typical miles cards usually give you 1.2-1.4 mpd.

Sounds great? Of course it is! However, as with all good things in life of course there is a catch to this: The points you can earn are capped. I will go through this in details in the next section.

2. Pay attention to a card’s Monthly (or Annual) points cap

All of the 10x cards have a points cap. Meaning, you cannot just charge a $5,000 spend and earn 5,000 x 4 = 20,000 miles from it. For example, the cap might be $1,000 a month. If you charge $5,000 to that card in one go, you’ll only earn 4 mpd on the first $1,000. I’ll get to the calculations in a bit.

Most cards have this cap as a monthly cap — which is a bit restrictive for a big spending, as getting a fridge would have already blown your monthly cap. However, some cards (such as OCBC Titanium) have it as annual cap — which is great for furniture spending!

This is definitely something you want to keep an eye on, as the consequences of going over the monthly cap could be dire. If you exceed a credit card’s points cap, you’ll only earn a measly 0.4 miles per dollar on your spending.

So going back to the example above: If you charge $5,000 to a card that has a monthly cap of $1,000, you’ll then earn 1,000 x 4 + 4000 x 0.4 = 5,600 miles. A far cry from 20,000 miles. If you had used your miles card instead, you could be earning 6,000 - 7,000 points!

Simply put, you will only earn bonus 10x points on spending that does not exceed the points cap, so you really want to pay attention to this and stagger your purchases if possible.

3. Keep an eye on when the points cap resets

So we have now learned that most rewards cards have a monthly cap — which means… it resets every month!

If you’ve bought a sofa and TV console for $1,700 this month using one card that has a limit of $2,000, then you’ll want to hold off on using that card for another big spend until the points cap has been reset.

However, the reset cycle differs from bank to bank. You definitely want to keep a check on this, especially when you are planning as big of a spending as furnishing a house.

Here are a few examples (not to be taken as facts! double check your card’s T&C!):

- For DBS, the points cap resets every calendar month, which means every 1st day of a month is a fresh start for your monthly points cap.

- On the other hand for Citibank, the points cap resets on statement month, and the statement month depends on when you open your card. Check with your bank for the exact dates.

Again, you’d want to check your card’s T&C for this, as rules change all the time.

4. Remember that points DO expire for these cards!

Unlike the miles card which often offers unlimited expiry, points do expire for the 10x rewards cards. And sometimes, the points expire very fast. DBS Woman’s Card for example, has only one year expiry which is extremely short. Citi Rewards on the other hand - points expire after five years, but they expire in block, meaning it’s possible some of the points you’ve just earned recently will expire soon if you’re nearing the 5 year mark of your card anniversary.

5. Ready to apply? Find out what the current sign up bonuses look like!

A lot of 10x cards offers similar benefit, so how do you choose which card to get? Sometimes if the options are pretty much on par, you’ll want to maximize your points earning further by taking advantage of any sign-up bonuses the card might be offering.

The catch is that most of these sign-up bonuses are only offered to new-to-bank customers, which means you cannot be the primary card holder of a credit card from the offering bank for the past 12 months. Make sure you read the promotion T&C for the qualifications, before applying for the credit card.

Also note that a card approval might take some time, so you’ll want to shortlist and apply for cards at least a month before your forecasted spending. If you have a good credit score and good credit track with a certain bank, you MIGHT be able to get it faster — I got my DBS and Citi card in 3 days. But if you’re a new credit card owner or a foreigner, this could take up to a month to process.

Example: My credit card stack for home furnishing & my purchase strategy

For my renovation spending, here are the cards I ended up getting. I’ve included a brief explanation on why I chose them and their weak points:

- DBS Woman’s World Card (Mastercard) — Good for online purchases. Monthly limit of $2,000 a month. The main benefit of this card is that they offer 10x Rewards on Travel. However, the big down side of this card is that the points expire after only ONE YEAR.

- Citi Rewards Card (Visa / Mastercard) — Good for online purchases. Monthly limit of $1,000 a month, which is a bit low. They also exclude bonus rewards on Travel purchases. TBH I got this card only because they had a sign-up bonus promotion and because I wanted to increase my monthly points cap. Otherwise, the DBS Woman’s World would have taken care most of the purchases! But in the end, Citi Rewards card became one of my regular card just because of how versatile it is.

- OCBC Titanium (Mastercard) — Good for online and offline purchases, but only for limited merchants. The main benefit of this card is the ANNUAL limit of $12,000 a month, which makes it THE perfect card for when you anticipate a big spending on home furnishing!

- DBS Altitude (Visa) — I use DBS Altitude as my everyday spend card and to catch any “spillover” dollars in case I exceed the monthly cap of all the cards above. TBH, it’s not the best in terms of miles per dollar (only 1.2 mpd), but it is a convenient choice for me since I already bank with DBS and I’ve been using this card for years. There are better cards out there that offers 1.4–1.6 mpd, if you don’t already have a miles card.

I mostly went for cards that rewards online purchases, since everything can now be bought online. So I would go visit stores like Castlery, IKEA, Best Denki, etc to see the stuff I want to buy. Then I go home and buy it online.

Stagger out your purchases

As you can see from the card stack list above, my monthly spending that will earn me bonus reward is capped to $3,000 (I’m not counting the OCBC Titanium cap, since it is quite limited). $3,000 is definitely not enough to furnish a 3 bedroom apartment, but the good news is — with home furnishing you often can stagger out your purchases… which is exactly what I did!

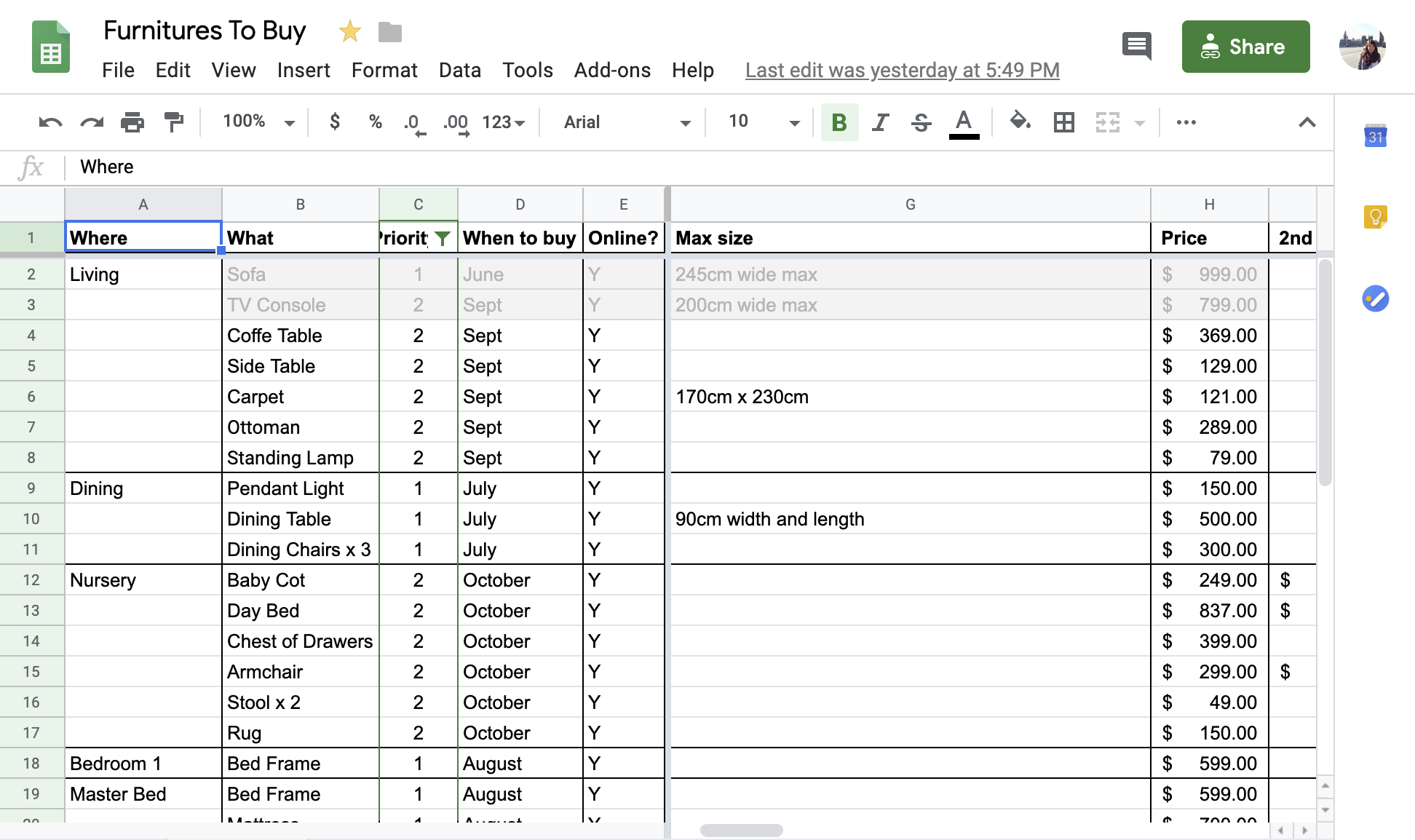

I made a spreadsheet of the main furnitures I anticipate we will need, and grouped them into months in which I will buy them based on need and forecasted price. For example, we definitely needed washing machine and fridge right away. But TV or TV console? maybe they can wait a little. This way, I made sure I spend somewhere close to $3,000 a month and will use the OCBC Titanium card for the spillovers.

Okay, that was a really long write up. I hope you’ve learned a thing or two from it. I have to leave you with this disclaimer: This strategy might not work for everyone, but I think it is the best for someone like me at the time being. So when you are researching for your cards, do take note if there is any new card in the market, whether the banks have updated their points rewards system or any ongoing sign up promos!

In some cases, you could even make your purchase months in advance and ask the supplier to deliver later. If I remember correctly, Castlery allowed us to do this.

I also want to thank my buddy Melvin Lim for inspiring and being my sounding board during the formation of my early strategy. If he hadn’t been doing this, I wouldn’t have even thought about getting into the points game!

And another special shoutout goes to my buddy Gherry, who is not at all a woman, but for letting me know about the benefits of DBS Woman’s World Card 😂

Additional Reading

Lastly, I’ll also leave you with some additional readings that have helped me. Hopefully, you will find them useful too!